With markets at all-time highs and most developed market governments bonds forecasted to continue at, or below zero yields, investors today are faced with a difficult question: How do I effectively hedge my portfolio?

Of course, this has always been a hard question to answer. Modern Portfolio Theory showed the world that by combining enough non-correlated assets into a diversified portfolio, the idiosyncratic ebbs and flows of each unique security or asset class can be moderated to lower overall portfolio risk. Correlations, however, are notoriously unstable and unpredictable in periods of market stress making portfolio construction a challenge in the best of times.

The risks investors face today are many and well publicized, including inflation risk, interest rate risk and credit risk, amongst others. Efficient market theory would suggest these risks are priced into markets, yet our behavioral biases often contribute to mis-pricing certain assets leading to market volatility when we least expect it. Such biases often find adoption of capital preservation strategies that have worked in the past, without considering that they just may not work in the future. While it is often impossible to predict the next market drawdown, there is one risk that we believe is under-appreciated by the market and could prove to be challenging to fixed income as well as equity markets: inflation.

Inflation

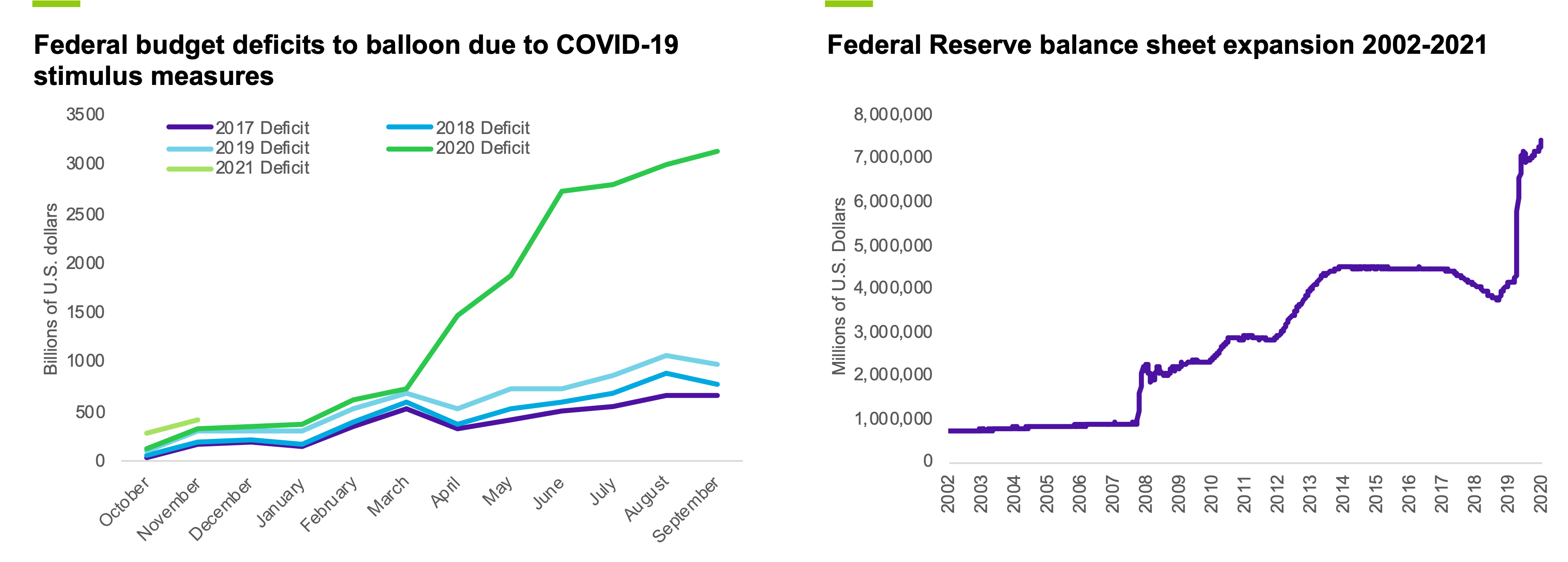

Inflation surprises tend to blow holes in portfolios and ultimately erode the purchasing power of an investor’s capital. While we do not see much inflation today, we believe that a sustained period of inflation (above the Fed’s stated mandate of a “normal” 2%) may be visible in the medium term. This expectation is evidenced by the following charts which outline the tremendous liquidity glut sustained by dual factors: a burgeoning U.S. fiscal deficit that will continue to grow, alongside massive and unprecedented expansion of monetary support via the Federal Reserve’s balance sheet (as well as central banks around most developed and emerging markets).

Left chart: U.S. Department of the Treasury, Congressional Budget Office as of November 30, 2020. Graph shows cumulative deficits over the fiscal year, which begins in October. Right chart: Federal Reserve Bank of St. Louis, as of December 31, 2020.

Inflation has the potential to cause wealth-erosion in portfolios as it can significantly decrease purchasing power. And with the massive amounts of monetary and fiscal stimulus currently flooded throughout world economies as seen above, we believe elevated levels of inflation may be upon us in the medium term. However, allocations to the following asset classes may potentially mitigate inflation risk:

- Commodities, such as gold and rice

- Inflation-linked bonds

- Inflation-aware equities

Commodities

Gold: Gold is the classic inflation hedge and has tended to rise in price with inflation since its first discovery. However, gold has proven to be more beneficial in certain types of economic environments than others. Gold does not provide an income stream to help buffer any losses in principal due to inflation. Rather, gold is a very effective “store of value,” and for that reason alone an allocation is prudent. Additionally, with rates at historical lows across the globe and a relatively weak U.S. dollar, we expect that gold should continue to be the better “safe play” than the greenback. In fact, in rising interest rate environments, the U.S. dollar tends to strengthen relative to gold due to its higher carry. However, the Federal Reserve continues to peg U.S. real rates securely between 0 and 25bps, broadcasting to the market that monetary policy will remain accommodative for the intermediate term, thereby providing a stable backdrop for gold.

Rice: The purpose of a rice allocation - accessed through the futures market - is not explicitly to guard against inflation, yet more for exposure to an essential commodity that is produced and consumed substantially in Asian markets that are poised to grow from a population and GDP perspective (China and India specifically). Additionally, as governments look to shore up food supplies, particularly in periods of supply chain disruptions and pandemic stress, rice may stand to benefit. In a weak U.S. dollar environment, we believe the price for rice should be intrinsically supported just as it is for other metals and commodities.

Inflation-Linked Bonds

Treasury Inflation-Protected Securities (TIPS) may provide strong inflation-protection as the income they generate is indexed to inflation. TIPS are Treasury bonds that, combined with the full faith and credit of the U.S. government, offer payments that adjust with the overall level of inflation as measured by the Consumer Price Index (“CPI”). They also maintain the same high quality “safe-haven” characteristics as their nominal (non-inflation adjusted) brethren, Treasury bonds.

Inflation-Aware Equities

As deep and wide as equity markets are, there are subsets of the asset class that provide strong “inflation-aware” characteristics. Our investment team often focuses on companies that exhibit maximum pricing power, with the ability to pass on higher input costs directly to the consumer in the form of higher prices. Sector examples include: Consumer Staples, Healthcare and Information Technology. Additionally, we look for equities with robust company business models, balance sheet strength, and free cash flows that may persist through inflationary periods. We believe companies that embody these high-quality characteristics may provide inflation-aware total returns over the long term.

A multi-asset ETF

With markets at or near all-time highs and interest rates at, or below, zero for much of the developed world, investors should consider investments that seek to address a variety of negative market scenarios. Given the unprecedented monetary and fiscal stimulus of governments around the world, we believe it is important that investors consider investments that replace or complement traditional hedges to an upside inflation surprise. Emles offers a fund that maintains strategic allocations to the asset classes discussed in this article. Among its many other defensive characteristics, the Emles Protective Allocation ETF (DEFN) includes assets which have traditionally helped to protect portfolios against inflationary shocks, as well as other systematic market risks, though, of course, nothing can protect entirely against loss. Therefore, a long-term allocation to DEFN may serve to improve portfolios' risk-adjusted total returns.

Tags: Capital Preservation, Commodities, Diversification, ETF, Inflation