Inflation surged over the past 12 months, as the consumer price index (CPI) rose 5.4% through the end of June, the largest 12-month increase since 2008, according to the U.S. Bureau of Labor Statistics.1 Sharp increases in the prices for used cars and trucks, larger-than-expected increases in food costs and a spike in gas prices were key contributors. Even without volatile energy and food prices in the mix, the CPI rose 4.5%, the largest 12-month increase since November 1991.

While U.S. Federal Reserve Chair Jerome Powell and Treasury Secretary Janet Yellen have been offering assurances that higher inflation will be temporary, the June CPI report raised concerns. With the delta variant bringing an increase in COVID-19 cases, expectations that the economy will benefit from a post-pandemic fueled surge have been at least somewhat tempered.

Higher prices appear to have shaken consumer confidence. The University of Michigan’s consumer sentiment survey dropped to a five-month low of 80.8 in July.2 The decline seems to have stemmed from consumers’ perceptions of diminished prospects for the economy and concerns about the rising prices on homes, vehicles and household durable goods.

Economists still optimistic about U.S. GDP growth

Even amid these slightly lowered expectations, however, economists remain confident that the United States will experience strong growth this year. In its monthly survey of economists, Bloomberg found that forecasts were for a 9.0% annualized rate of increase in U.S. gross domestic product (GDP) for the second quarter, followed by a 7.1% gain in the third quarter, and a 5.1% annualized GDP increase in the fourth quarter.3 The projected growth rate for all of 2021 is 6.6%. If growth does achieve that level, it would make 2021 the second-best year for U.S. economic expansion since 1966.

Pent-up demand for restaurant dining and traveling – after more than a year of consumers having severe restrictions on all outside-the-home activities – is expected to be one key driver of those economic gains.

Delta variant takes hold

A July 22 report from Johns Hopkins University showed there were 43,700 new COVID-19 cases per day in the United States over the previous week.4 It was a 65% increase from the previous seven days, and three times higher than the level seen two weeks earlier. Louisiana, Arkansas, Missouri, Florida and Nevada reported the highest averages of new cases per capita, at rates double the overall level for the United States.

The increase in cases led the Centers for Disease Control to reverse its recent recommendations on mask-wearing. It is now advising even those who are already vaccinated to resume wearing masks indoors. With the exception of one-day market disruptions when particularly concerning news about the delta variant is released, the financial markets overall seemed to be taking in stride the stalled progress in putting the pandemic fully behind us.

Reports from Israel, where the delta variant is now the dominant strain of the COVID-19 virus also suggest the Pfizer and BioNTech’s COVID-19 vaccine may be only 39% effective. Even though it may not eliminate the risks of getting the virus, the country’s Health Ministry did stress that the vaccine still provides strong protection from COVID-19-related severe illness and hospitalization.5

Higher-than-expected jobless claims

The advance number for seasonally adjusted initial jobless claims was 419,000, an increase of 51,000 from the previous week.6 In our view, some abnormal influences might have caused this break in what had been an improving trend. Among these factors may be the adjustments auto manufacturers have had to make in their labor forces. The car companies are dealing with the impact on their production lines of the ongoing shortage in semiconductors, a critical component in today’s highly electronic cars.

It’s also important to note that the jobless claims are significantly lower than they were at the height of the pandemic, even though the pace of improvement has slowed.

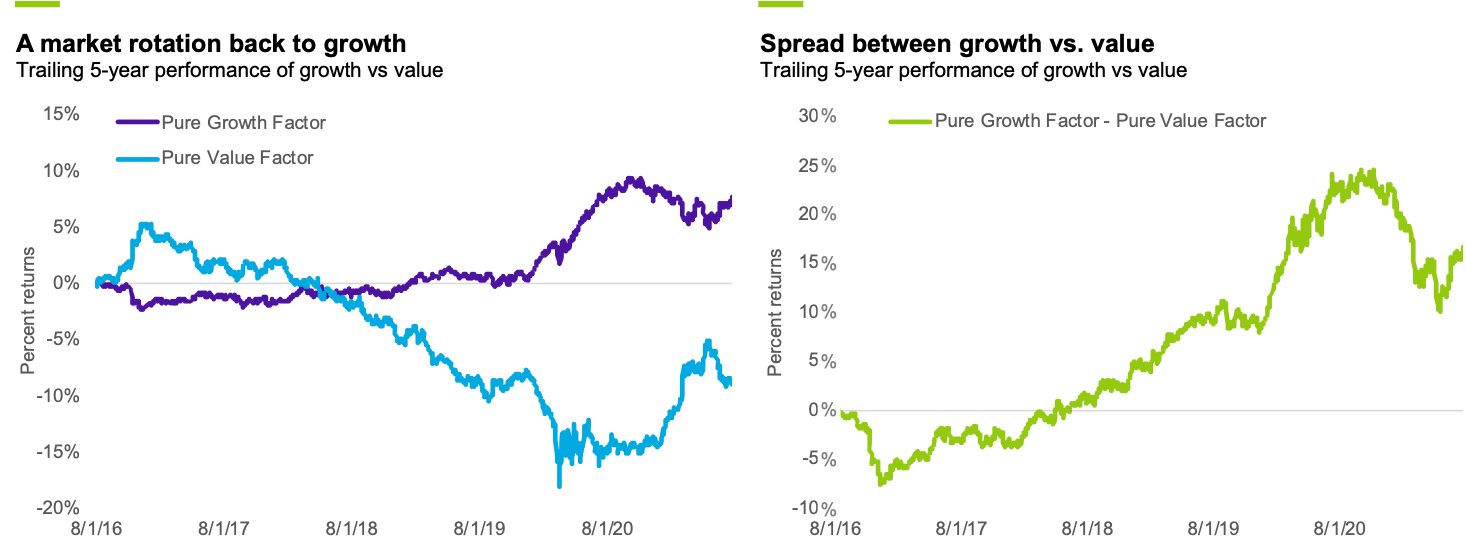

A market rotation back to growth

The consistent gains in the U.S. stock market in recent months have come from large-cap growth stocks. Prices on small-cap growth stocks, as well as large- and small-cap value stocks, have been mildly correcting since May.

After so many years of dominance by growth stocks, the rotation back to value began last year. The recent reversal back to growth likely stems from doubts about whether the conditions that favor value stocks are in place. These include consistently strong GDP growth, higher interest rates, and a distinct end to the pandemic.

Source: Bloomberg, data as of July 29, 2021. Pure Growth Factor as defined as the PGRWTHUS Index. Pure Value Factor as defined as the PVALUEUS Index.

Bipartisan infrastructure bill advances

On Wednesday, July 28, the Senate voted to advance a $550-billion infrastructure bill. The vote was 67-32, with 17 Republicans and all 50 Democrats voting yes.7 The bill’s spending proposals will focus on transportation, broadband and utilities. The Democrats hope to pass the infrastructure plan along with a second bill that would spend $3.5 trillion to expand social programs. House Speaker Nancy Pelosi of California has said the House of Representatives will not take up either bill until the Senate passes both.

The bipartisan agreement on the bill was reached after a decision to help pay for it by delaying the effective date of a proposal from the Trump administration. The proposal had been to replace safe harbor protections for drug rebates in Medicare Part D with discounts for consumers at the pharmacy counter. Critics challenged the rule, saying it might not work as intended and could increase drug costs for everyone. The Congressional Budget Office estimated that implementing the rule would increase federal spending by $179 billion through 2029.

Senate progressives take aim at Fed Chair Powell

Jerome Powell’s current term as Chair of the Federal Reserve will end in February. This month, Senators Sherrod Brown of Ohio and Elizabeth Brown laid out a list of complaints about Powell’s decisions at the Fed.8

Senator Brown said he has liked what has been done with monetary policy, but does not like what has been done with regulation, particularly with what he perceives as a weakening of banking regulations. While the Biden Administration has not given any indication of which direction it may be leaning, the support of key Democratic senators will be critical for the Fed chair appointed by former-President Trump to receive a second term.

Regulations of cryptocurrencies may be coming

As The Wall Street Journal reported, Treasury Secretary Yellen will be meeting this month with the Fed and the Securities and Exchange Commission to discuss stablecoins.9 These digital currencies, which are used to facilitate transactions with cryptocurrencies like bitcoin, are pegged to national currencies like the U.S. dollar. They are now being seen as a potential risk not only to cryptocurrency markets, but also to capital markets.

Secretary Yellen says the meetings will help regulators assess the benefits of stable coins, while also determining how to mitigate the potential risks they present to users, markets and the financial system.

ECB plans to stick with monetary stimulus

The European Central Bank (ECB) announced this month that it will keep its monetary stimulus efforts in place even longer, even if inflation shows some temporary spikes.10 In effect, that means the ECB will likely continue buying assets well after the Fed has tapered its Quantitative Easing program. The ECB said its goal is to keep consumer prices increasing “durably” at 2%. Given that, it appears unlikely that the ECB will increase interest rates until 2023. The central bank also said it would strive to use its influence on the bond market to address climate change.

Enjoying our market recap? Subscribe to our insights to receive timely market updates.

Tags: Inflation