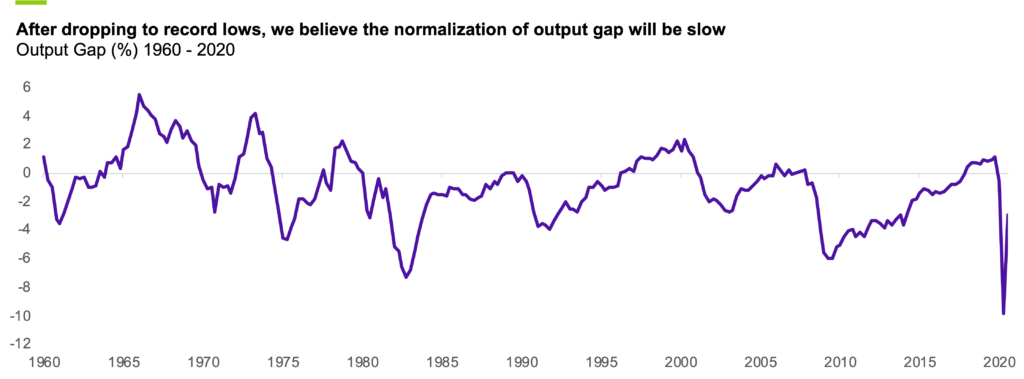

Over the last two decades, moderate GDP growth, negative output gap and the deflationary impacts of globalization have kept U.S. inflation at bay. While record levels of monetary and fiscal stimuli would ordinarily spur inflation, low output gap and employment numbers have kept policy activism from translating into higher prices. Part of this is driven by the “Amazon” effect, which has shifted pricing power towards consumers. But more importantly, the traditional relationship between an increase in money supply and corresponding increases in consumption, business investment, wages and prices has been upended. Instead, the velocity of money has plummeted to historically low levels, resulting in asset price inflation in financial markets rather than Consumer Price Index (“CPI”). Yet, investors respond to expectations ahead of reality - and inflationary concerns, a steepening yield curve and imminent fiscal stimulus are increasingly top of mind.

Source: Bloomberg, data as of December 31, 2020

Look for persistence

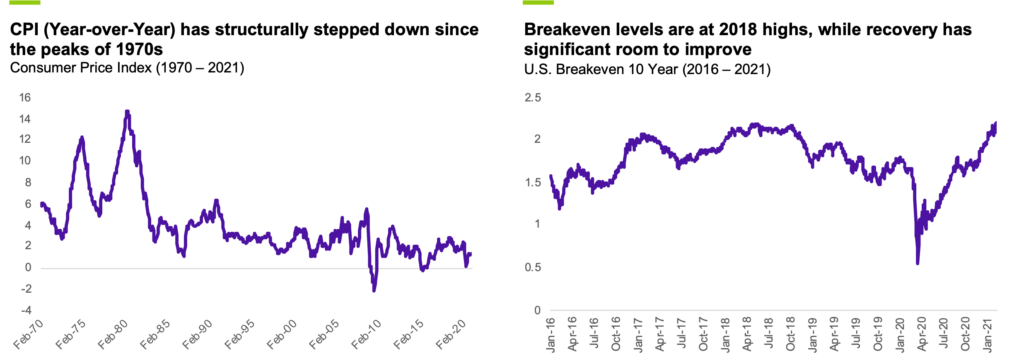

In our view, rather than a binary month-over-month rise or fall in inflation, it is the rate of change and the persistence of CPI that matters most. “Tantrums” created by inflationary spikes and the Fed’s reactions to them are more of a risk to economy and markets than tepid, anticipated inflation and Fed moves. Quoting from our Annual Outlook, we continue to view inflation to stay low over the near-term, with natural base effects pushing Year-over-Year (“YoY”) numbers higher as March and April 2020 drop off in the calculations. Over the mid-long term and as fundamental data strengthens, inflation should gently rise and persist at or above the Fed’s 2% target. The CPI numbers released on February 10, 2021 indicate a 1.4% rise in headline CPI, below the 1.5% estimate survey level. The CPI changed 0.3% Month-over-Month, slightly lower than the 0.4% of the prior reading. Among the constituents of the headline index, the outlier was a steep 7.4% jump in gas prices following the surge in oil since November. More broadly, this caused a marginal drop in bond yields which were anticipating a step up in inflation data.

To us, this means that the Fed’s clear mandate on accommodative monetary policy will continue until “substantial further progress” on employment and “persistent” 2% inflation occurs. In the current blue regime, political policy will prioritize economic recovery from the pandemic, acknowledging its far-reaching effects on workers and businesses. The recent softer employment data released on February 5, 2021 furthered the case for fiscal stimulus. While equities tend to fare well in periods of modest inflation (1-3%), investors should be vigilant to future-proof their portfolios, particularly the credit portion, for inflation and duration risk as we navigate reflation and volatility risks.

Source: Bloomberg, data as of February 2, 2021

Tags: Inflation